FIRE Explained Simply: A Practical Path to Financial Independence

FIRE stands for Financial Independence, Retire Early. Most explanations focus on saving a large percentage of income and investing slowly over decades.

That approach may work, but for many people it creates a long timeline, high stress, and delayed lifestyle flexibility.

At Power Couple Financial Coaching (PCFC), we take a different approach:

Fix cash flow first

Use growth to do the heavy lifting

Apply structure as your portfolio grows

Build flexible income over time

This page explains the framework. PCFC tools are designed to help you apply it.

What Most FIRE Advice Gets Wrong

Many traditional FIRE models rely on two ideas:

Save a high percentage of income

Reach ~25× your annual expenses

That 25× number comes from the 4% rule.

The 4% rule does adjust for inflation, but it still assumes:

withdrawals happen every year regardless of conditions

the portfolio stays largely static

no meaningful strategy adjustments are made

It’s not that the 4% rule is wrong. It’s that it assumes you don’t adapt.

The PCFC Framework: A Step-by-Step Path

Instead of focusing on one number, PCFC uses a progression.

Phase 1: Fix Cash Flow (Foundation)

Before investing becomes the focus, stability matters.

Goal:

Become cash-flow positive

Build a basic emergency reserve

Reduce reliance on debt

Without this step, everything else becomes fragile.

Use our free tools to:

track spending

eliminate negative cash flow

build a stable base

Phase 2: Grow to ~5× Expenses (First Real Milestone)

Most people believe they need the full FIRE number before life improves.

PCFC takes a different approach.

Instead of aiming for 25× first, focus on reaching about 30% of your target range.

16.6×0.30≈5

This means:

You are aiming for roughly 5× your annual expenses first

Why 5× Matters

At around 5×:

You are no longer starting from zero

Growth begins to have meaningful impact

Financial pressure starts to decrease

You gain flexibility in how you work and live

The goal is not to wait until the finish line. The goal is to improve your life along the way.

Why Growth Must Do the Heavy Lifting

If financial independence is the goal, there are only three levers:

how much you save

how fast your portfolio grows

how long it takes

Most FIRE advice focuses heavily on saving.

PCFC places more emphasis on growth in the early phase.

The Reality of Slow Growth

Using only traditional broad-market exposure may work over long periods.

However, slower growth often means:

needing a higher final target

contributing for more years

delaying flexibility

The PCFC View on Growth

Some investors choose to include higher-growth exposure during the early accumulation phase (for example, leveraged index exposure concepts such as QLD or SSO).

The goal is not speculation.

The goal is:

Allow growth to do more of the work so the required savings and timeline may be reduced.

What to Do in This Phase

Stay consistent with contributions

Accept volatility as normal

Avoid emotional decision-making

Focus on growth, not income

During this phase, the risk is often not the asset. The risk is abandoning the plan.

What Happens After 5×: Structure and Control (TAS)

Once your portfolio reaches meaningful size, the problem changes.

Early on:

You are trying to grow.

Later:

You are trying to avoid losing years of progress.

The Problem Most Investors Face

Traditional approaches often stay fully invested at all times.

This means:

large drawdowns are accepted

recovery can take years

progress may stall

The PCFC Solution: TAS

PCFC uses a structured system (TAS) to address this phase.

The goal is not to predict every move.

The goal is to:

participate in stronger market conditions

reduce exposure during weaker periods

follow rules instead of emotion

Avoiding large losses can be just as important as capturing gains.

Why This May Matter

Over time, reducing large drawdowns may:

preserve capital

shorten recovery periods

improve long-term outcomes

Why PCFC Uses a Different Target Range

Traditional FIRE discussions often reference a target around 25× annual expenses. That number comes from the 4% rule, which is based on historical studies using fixed withdrawal strategies over long periods.

Those studies were designed to answer a very specific question:

“What withdrawal rate would have survived past market conditions using a largely fixed approach?”

That is useful information. But it is not the only way to approach financial independence.

What the 25× Framework Assumes

The traditional model generally assumes:

withdrawals continue every year, adjusted for inflation

the portfolio remains largely static

limited adjustment based on market conditions

no structured approach to managing major drawdowns

It is a model built around consistency, not adaptability.

The PCFC Approach

PCFC uses a different framework built around:

growth doing more of the work early

structured decision-making as the portfolio grows

reducing large drawdowns when possible

adapting to changing conditions over time

Instead of aiming for one fixed number, PCFC often discusses a range around ~16× as a point where:

income can be supported from multiple sources

growth can continue

decisions can be adjusted over time

Core Idea

This is not about accepting less safety. It is about using a different system.

Why This Works Differently

The PCFC framework does not rely on a single assumption.

It considers:

higher-growth phases earlier in the journey

structured approaches to manage risk (such as TAS)

the ability to adjust withdrawals, income sources, and exposure

changing environments, including interest rates and yields

Outcomes are influenced by decisions over time, not just one starting number.

A Comparison

25×:

based on fixed historical modeling

designed to work without changes

16× (PCFC framework):

based on growth + structure + adaptability

designed to be actively managed over time

Final Thought on This

The difference is not certainty versus risk. The difference is a fixed system versus an adaptive one.

Using Yield When It Makes Sense

In some environments, lower-risk instruments such as CDs or Treasuries offer meaningful yields.

When that happens, some investors choose to:

allocate a portion of their portfolio to those instruments

generate part of their income from yield

reduce the need to sell growth assets

If part of your income is covered by yield, the rest of your portfolio has more flexibility to grow.

Important Considerations

yields change over time

inflation affects real returns

conditions are not constant

This is why flexibility matters more than fixed rules.

The Real Risk Most People Miss

Risk is often described as volatility.

In practice, risk is often behavior.

Examples:

abandoning a plan during normal volatility

reacting emotionally to market movement

switching strategies repeatedly

selling at the wrong time

The investor’s behavior often matters more than the asset itself.

Putting It All Together

The PCFC path:

Phase 1: Fix cash flow

Phase 2: Grow to ~5×

Phase 3: Apply structure (TAS)

Phase 4: Reach flexible financial independence (~16× range)

Most plans focus on getting you there eventually.

PCFC focuses on getting you there sooner, while maintaining control along the way.

Phase 1 PCFC Financial Decision Tools

Phase 1 — Foundation

Fix cash flow, build savings, and stop financial stress

Phase 2 — Growth

Start building assets and learn how investing actually works

Phase 3 — Protection

Protect what you’ve built and avoid major financial mistakes

Phase 4 — Income

Turn assets into income while continuing to grow

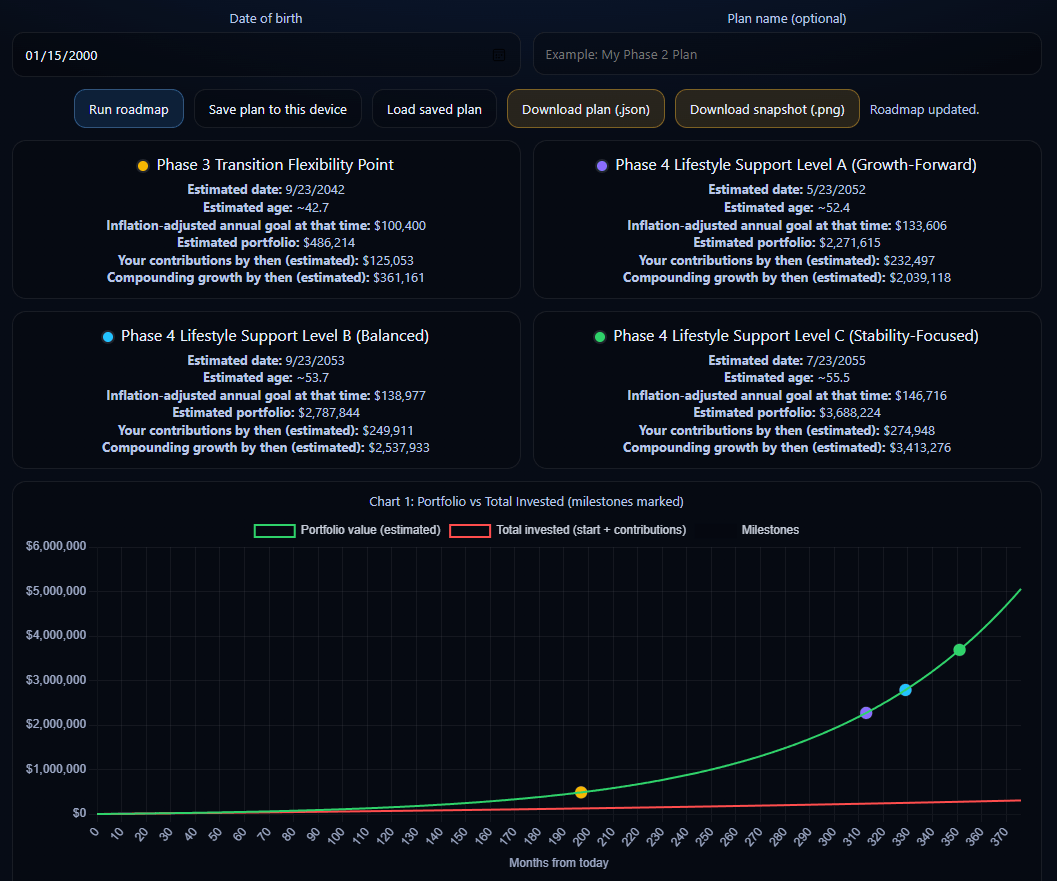

Phase 2 PCFC Financial Freedom Roadmap Calculator

The image below is an example view from the PCFC Financial Freedom Roadmap Calculator.

This tool helps map your progress, estimate phase transitions, and show how contributions and growth work together over time.

It is one of several tools included inside the PCFC Complete System.

Power Couple Financial Coaching provides educational information only. Nothing on this page constitutes financial, investment, tax, or legal advice. All investments involve risk, including loss of principal. Examples are illustrative only and not guarantees of future results.